A sector refers to a group of stocks representing companies in a similar line of business. The Global Industry Classification Standard (GICS) set out by Standard & Poor’s and Morgan Stanley Capital International classify stocks into 10 sectors, which in turn are divided into industry groups, industries and sub-industries.

|

Sector |

Description |

|---|---|

|

Financials |

Primarily composed of banks, credit unions, insurance and mutual fund companies. |

|

Energy |

Composed of companies engaged in the exploration, production, marketing, refining or transportation of oil and gas products. |

|

Materials |

Made up of companies in a wide range of commodity-related manufacturing and mining industries, including metals, minerals, chemicals, construction materials, glass, paper and forest products. |

|

Industrials |

Made up of companies whose businesses are dominated by one of the following: aerospace and defense, construction, engineering and building products, or transportation services including airlines, rail, and transportation infrastructure. |

|

Consumer Discretionary |

Industries included: automotive, household durable goods, textiles, apparel, and leisure equipment. The services segment includes hotels, restaurants, leisure facilities, media production/services, and consumer retailing. |

|

Telecom |

Made up of companies that provide communications services primarily through fixed-line, cellular, wireless, high bandwidth, and/or fibre-optic cable networks. |

|

Information Technology |

Comprised of companies in the following three general areas: technology, software and services. |

|

Consumer Staples |

Includes manufacturers and distributors of food, beverages, and tobacco, as well as producers of non-durable household goods and personal products. It also includes food and drug retailing companies and consumer supercenters. |

|

Utilities |

The sector is made up of electric, gas, and water utility companies as well as companies that operate as independent producers and/or distributors of power. |

|

Health Care |

Includes companies that manufacture health care equipment and supplies or provide health-care related services. It also includes companies who are primarily involved in the research, development, production, and marketing of pharmaceuticals and biotechnology products. |

Sectors are relevant to stock selection because different sectors will behave differently depending on the state of the local and global economy.

In fact, some macroeconomic events can affect a sector in a direct or indirect way. For example, if the international price of oil falls, all companies that explore for, produce, transport or market oil will earn less money, as will the companies that sell them goods and services. It is therefore important to diversify your portfolio by sector in order to reduce sector-specific risk.

Analyze Your Portfolio

In addition to showing your account's or goal's mix of cash, fixed income and equities, the Analyze & Rebalance tool can also analyze your sector and regional exposures. You can verify whether you are under or over-concentrated in any holdings, and then determine your portfolio risk.

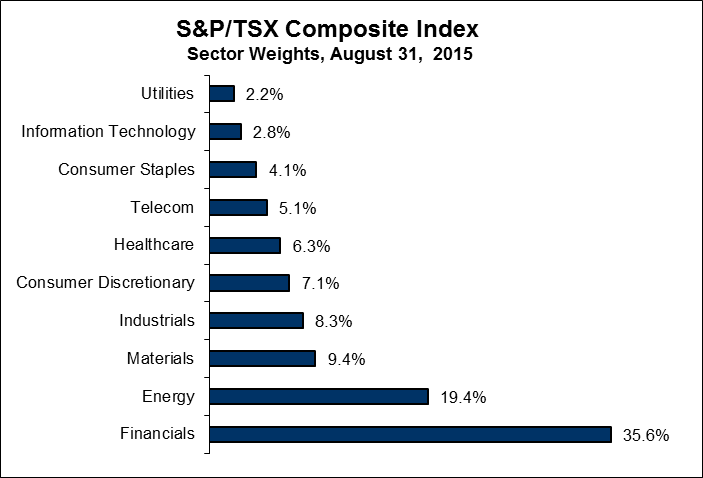

As you can see from the pie chart below, the financial and energy sectors dominate the Canadian landscape, with more than 50% of the S&P/TSX Composite Index made up of companies in these sectors. The materials sector is also quite large, and these three sectors together represent over 60% of the companies in the index. Meanwhile, the small weightings of health care, utilities and consumer staples provide very little domestic exposure to these important sectors.

A table presenting individual sector weightings on the S&P/TSX Composite Index as of August 31st 2015

Sector Weight

Utilities 2.2%

Information Technology 2.8%

Consumer staples 4.1%

Telecom 5.1%

Healthcare 6.3%

Consumer discretionary 7.1%

Industrials 8.3%

Materials 9.4%

Energy 19.4%

Financials 35.6%

If you’re interested in a sector perspective, you may appreciate the information available on the Sectors & Industries page. You’ll find the performance and fundamental data for different sectors and industries in both Canada and the United States. Industries are a sub-category of sectors which you can explore in depth to find specific companies operating in each industry. For example, you can research the dividend yield, price to earnings ratio (P/E) or one-year return of Canadian natural gas utilities as a whole or research individual companies.

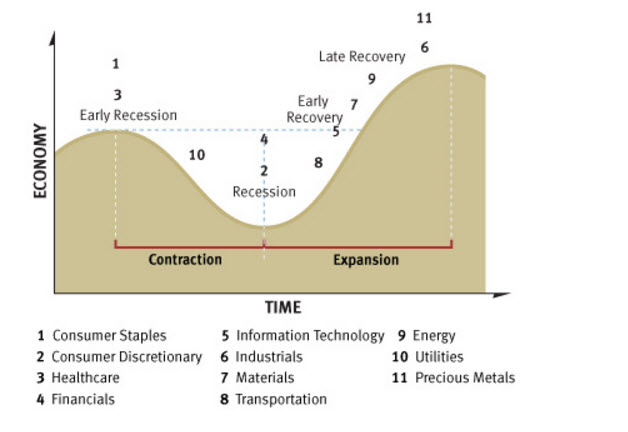

Sector rotation is an investment strategy that consists of moving money from one sector to another in an attempt to beat the market. Over time, an economy goes through periods of growth (i.e. expansion) and periods of contraction (i.e., recession). Economic growth typically benefits certain sectors, known as cyclical sectors, while less economically sensitive (or non-cyclical) sectors perform better during harder times. Non-cyclical sectors are also known as defensive sectors, because their stable dividends and earnings are regarded as a defense against stock market declines (although no stock is immune to an economic downturn). As the economy changes, therefore, an investor may choose to shift investment assets from one sector to another.

Business Cycles and Cyclical Sectors

A period with one recession and one expansion is known as a business cycle. This cycle can be broken down into four parts, each of which is associated with the outperformance of certain sectors.

Early recession: The economy begins to slow, as measured by gross domestic product (GDP) , and consumer expectations are at their worst. Industrial production is falling sharply, interest rates are at their highest and the yield curve is flat or even inverted (meaning that long-term interest rates are equal to or lower than short-term rates). Historically, the following sectors have profited during these times:

- Consumer staples, such as food producers and grocery retailers (near the beginning)

- Health care

- Utilities (midway)

Recession: Economic growth is down (i.e., GDP is contracting), and industrial production is at its lowest point. The unemployment rate is high. Interest rates begin to fall, and the yield curve is normal (meaning that long-term rates are higher than short-term rates). Although consumer expectations are low, they are beginning to improve. The sectors that have historically performed well in this stage include:

- Consumer discretionary, such as car manufacturers and clothing retailers (near the beginning)

- Financials

- Information technology (near the end)

Early recovery: The economy begins to improve, and consumer expectations continue to rise. Industrial production begins to grow. Interest rates reach their lowest point, and the yield curve is either normal or has begun to steepen (meaning long-term interest rates are increasing relative to shorter-term rates). The sectors to consider investing in at this stage include:

- Financials (near the beginning)

- Transportation (near the beginning)

- Other industrials

- Energy (near the end)

Late/full recovery: At this point in the business cycle, interest rates are usually rising rapidly and the yield curve has flattened. Industrial production is slowing and consumer expectations are beginning to fall. Historically, the most profitable sectors in this stage have included:

- Energy (near the beginning)

- Materials, including precious metals

Sector Period in which the sector tends to outperform

Consumer Staples Early recession

Healthcare Early recession

Utilities Midway through recession

Financials End of contraction

Consumer discretionary End of contraction

Transportation Early recovery

Information technology Midway through recovery

Materials Late recovery

Energy Late recovery

Precious metals End of expansion

Industrials End of expansion

1. Consumer Staples

As the term “staples” suggests, consumer staples companies usually experience fairly steady demand for their products and are therefore less sensitive to changes in the business cycle. These non-cyclical stocks attract investors when the economic cycle or bull market has matured, or when the market is beginning to contract.

2. Consumer Discretionary

Again, as the term “discretionary” suggests, this sector produces products consumers choose to buy (or not to buy), rather than products they need. Therefore this sector tends to be the most sensitive to economic cycles and interest rates. These stocks usually become popular when the economy is in its last stages of contraction , and consumer sentiment is improving.

3. Health Care

The health care sector is considered defensive, meaning companies in this sector are generally unaffected by economic fluctuations.

4. Financials

When interest rates are falling, stocks in housing-related industries often do well , so they are popular among investors in the middle to late stages of an economic contraction. Large banks that do not depend on mortgages alone are generally helped by commercial and consumer loan growth.

5. Information Technology

Technology stocks are often very cyclical. The companies depend on capital spending and business or consumer demand, which can be quite finicky. The stocks may also have long-term growth potential as new technologies are developed. Technology stocks are usually popular during the early to middle stages of an economic expansion .

6. Materials

Basic materials stocks tend to receive a boost from the market late in an economic expansion. Basic materials companies are strongly affected by the global economic picture and supply/demand metrics have a significant impact on stock price movements.

7. Industrials

As the economy begins to improve, capital spending tends to increase as higher demand for products leads companies to expand their production capacity.

8. Transportation

Railroads, trucking companies and other surface carriers tend to react positively when the economy starts to improve. Airlines, however, are more tied to cyclical fuel costs and competitive pressures.

9. Energy

These stocks tend to be popular with investors late in the business cycle and are driven by the global supply/demand picture for energy, although political events also tend to affect these industries.

10. Utilities/Telecommunication Services

Utility companies are sensitive to interest rates because of the large debt financing costs they must incur in order to build their infrastructures (such as power plants and pipelines). These stocks tend to perform well when interest rates are declining. Telecommunication services companies may also profit during these times.

11. Precious Metals

Precious metals (e.g. gold, silver and platinum) and the companies that mine and process them are largely affected by inflationary pressure and commodity price volatility. They are also affected by industrial and consumer demand. Investors often flock to this subset of the materials sector late in the expansion cycle.

View Legal Disclaimer

RBC Direct Investing Inc. and Royal Bank of Canada are separate corporate entities which are affiliated. RBC Direct Investing Inc. is a wholly owned subsidiary of Royal Bank of Canada and is a Member of the Investment Industry Regulatory Organization of Canada and the Canadian Investor Protection Fund. Royal Bank of Canada and certain of its issuers are related to RBC Direct Investing Inc. RBC Direct Investing Inc. does not provide investment advice or recommendations regarding the purchase or sale of any securities. Investors are responsible for their own investment decisions. RBC Direct Investing is a business name used by RBC Direct Investing Inc. ® /

™ Trademark(s) of Royal Bank of Canada. RBC and Royal Bank are registered trademarks of Royal Bank of Canada. Used under licence.

© Royal Bank of Canada 2017. All rights reserved.